Designing a Fund to support energy efficiency

Cost-saving investments are of interest to all businesses; reducing greenhouse gas emissions are of interest to everyone. This blog post is part of a series that summarises our 2016 Pre-feasibility Study, conducted with Arup, of a Fund to support energy efficiency investments by Cambodian SMEs.

Our research and analysis of possible energy efficiency solutions and their returns, as well as analysis of banking in Cambodia, determined that investing in EE solutions is profitable and that local banks do not lack liquidity. Furthermore, SMEs have the capacity to borrow (but often not the collateral). Generally, the returns from investing in energy efficiency can service debt at market interest rates. Hence, concessionary lending not required in a Fund to support energy efficiency (EE) investments.

Barriers and solutions to improved energy efficiency

Yet Cambodian SME are not investing in EE, despite its profitability. There are two causes of this, and our Fund design has two corresponding solutions, as shown here:

Investing in EE involves an upfront capital cost. Many SME need external finance for this. Yet Cambodian banks require collateral before they will lend. By providing a guarantee that acts as collateral, our proposed Fund overcomes this barrier.

The EE market in Cambodia is constrained. There is an absence of knowledge about EE solutions and their suppliers. Trust is also a problem, with little accreditation, regulation and legal recourse. Fees earned by the Fund can be used to overcome these issues in the EE market, via a Technical Support Facility. This facility can subsidise energy audits, certify/accredit suppliers, provide training, and market the benefits of EE solutions.

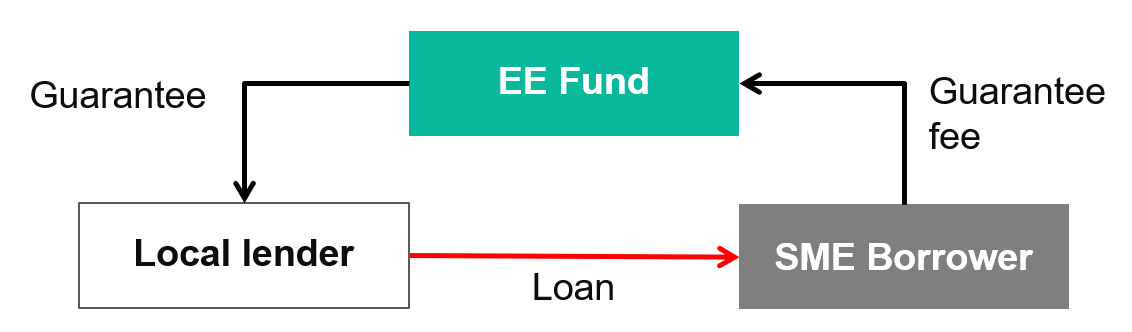

How the Fund works

The diagram below is a simple illustration of the guarantee system. The Fund provides the guarantee, for which the SME pays the Fund a fee. This fee covers Fund costs as well as the Technical Support Facility outlined above.

In our model of the Fund, the SME ‘pays’ 12% for a uncollateralised loan comprising;

- 6% credit fee for guarantee to Fund -> fund revenue

- 6% loan interest to the bank -> bank revenue

The 6% paid to the bank approximates bank average interest rate spreads, so there is minimal change for banks. Credit assessment and verification is completed by Fund, so minimal marginal cost to bank.

The model means multiple banks can participate (guarantees are “portable”), rather than a Fund linked to a specific bank. This is best practice in Fund design of this nature.

The benefits of our proposed model:

- Impact:

- ‘Built In’ additionality

- Leverages private sector funds

- No subsidies – no market distortion

- SME pays a ‘commercial’ effective rate

- Doesn’t subsidize any bank

- Facilitates deployment of existing market capacity

- Possibility of working with more than one bank – constitutes best practice

- Bank processes don’t have to change at all

- Possibility of self-funded Technical Support Facility

- Sustainable – the Fund generates a positive internal return (see below).

Results

Based on our analysis of the costs of typical EE solution, the number of SME in our target industries (only certain industries were studied, see here for details) and an assumed penetration rate, we were able to determine the number and amount of loans – and hence guarantees – required: 1,886 loans totaling $32 million.

We produced a full financial model of the Fund and estimated an IRR on initial capital of 7.1%.[1] We also estimated average greenhouse gas reductions of 92 tonnes carbon equivalent per loan. These results are summarised in the figure below.

The above results assume:

The above results assume:

- Fund life of 20 years, 5-year ramp up

- Market penetration of 30% in selected industries

- Loan terms

- Interest rate: 12% p.a.

- Loan tenor: 7 years

- Guarantee

- Interest rate to SME: 12%, incl. guarantee fee of 6% p.a.

- Loan default rate of 1.4%, with LGD of 20%.

We believe our Fund design would successfully leverage private sector capabilities and achieve significant impact (in GHG emissions reductions and in an improved EE solution market). The design ensures the sustainability of arrangements post the life of the Fund.

Energy efficient technology helps improve competitiveness and the environment. Our earlier blog posts described the relevant institutional environment in Cambodia, and the energy mix in Cambodian industry.

Other related EMC posts:

Challenges with Rice Husk Gasifiers in Cambodia

Select relevant reports from our client and their knowledge platform:

The Economic, Social and Environmental Impacts of Greening the Industrial Sector in Cambodia (pdf)

Cambodia’s Green Growth Potential

Exploring Financial Policy and Regulatory Barriers to Private Climate Finance in South-East Asia

[1] We also analysed a Fund model of providing loans direct to SME. This has a much lower IRR than the guarantee model.

Comments are closed.