Giving Credit Where Credit’s Due..

World Bank Doing Business Cambodia has barely budged with overall ranking declining slightly from 131 to 135 (2017 v 2018).

There are many things of interest to comment on in WB DB stats. What’s particularly interesting, for purposes of this post, is Cambodia’s extraordinary performance in the metric ‘Getting Credit’, where it scores 20th of 190 economies world-wide. That is ahead of not only the Mekong family (Lao PDR 79, Myanmar 177) but wealthy ASEAN cousins (Singapore, 29) and my home country (United Kingdom, 29).

This happens to be of interest because we’re frequently involved in ‘access to finance’ projects – the challenges of Cambodian SME to obtain credit from banks. Does this score accurately reflect how easy it is to get credit in the Kingdom? On another measure – ration of SME bank credit to GDP Cambodia doesn’t do very well at all! That’s possibly the subject of a later post…

What’s also interesting is how the stellar score on Getting Credit underpins Cambodia DB performance in general.

‘Doing Business Cambodia’ actually improved (a little)

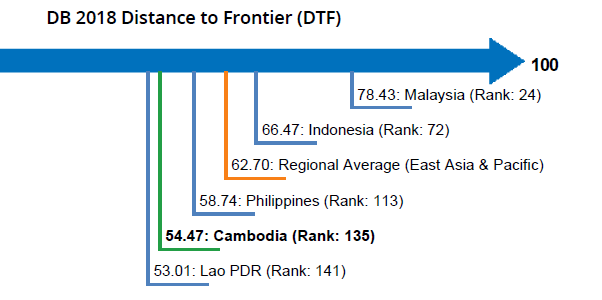

Rankings are what get talks about – a smart ‘nudge’ by the WB Doing Business team. However, rankings are derived from ‘Distance to Frontier’ (DTF) scores which show how much the regulatory environment for local entrepreneurs in an economy has changed over time in absolute terms.

The DTF scores for each metric are summed, to get an aggregate score, which is then compared to 190 economies to get the WB global ranking.

It’s of some interest that therefore whilst Cambodia ranking declined slightly (131 to 135) it’s DTF score rose very slightly (54.24 to 54.47).

Giving credit where credit’s due…

Cambodia’s Getting Credit is a great outlier compared to Cambodia’s performance in other DB metrics and made a major positive contribution to Cambodia’s DTF.

Cambodia’s DTF ranges from Getting Credit (80) to Enforcing Contracts (32.6). Including Getting Credit the average score across all metrics is 54.47. Excluding Getting credit the average DTF score falls to 51.63

That might not seem a lot, however, if we experiment, by adjusting the Getting Credit DTF from 80 to the 51.63 average (i.e. if ‘Getting Credit’ performed as well as other metrics) then the impact on the Kingdom’s ranking is big; Getting Credit DTF score itself calls from 20th to 89th and composite ranking falls from 135th to 147th (vs Lao PDR 141).

If RGC ‘Getting Credit’ score plummeted to the same level as, say, ‘Enforcing Contracts’ (32.67), then our average DTF falls to 49.73, and a ranking of 153th.

| Variable | Change | Impact on DB Ranking | ||

| From | To | From | To | |

| Getting Credit | 80.00 | 51.63 | 135 | 147 |

| Getting Credit | 80.00 | 32.67 | 135 | 153 |

| Enforcing Contracts | 32.67 | 56.89 | 135 | 123 |

The above also shows that if ‘Enforcing Contracts’ somehow to rose to the average of all other metrics (from 32.67 to 56.89) the resulting boost would see Cambodia rise to 123rd .

Impact of further improvements to ‘Getting Credit’

Getting Credit WB DB DTF score has been high ever since the RGC successfully implemented the Credit Bureau of Cambodia; 75 v 80 (2014 v 2018).

However, there are still 4 items for which Cambodia received ‘null point’ listed below. Collectively they account for 20/100, meaning if all measures were implemented to the satisfaction of WB DB Team they would lift Cambodia to a perfect score of 100/100. This would place Cambodia #1 in the world for ‘Getting Credit’ (!!!) and boost its overall WB DB ranking to 125th.

Legal Rights in Cambodia 10/12

This applies to legal rights for creditors, rather than rights in general, and focusses on the regulation of secured transactions. Cambodia’s ‘gaps’ are:

- Are secured creditors paid first (i.e. before tax claims and employee claims) when a business is liquidated?

- Are secured creditors subject to an automatic stay on enforcement when a debtor enters a court-supervised reorganization procedure? Does the law protect secured creditor rights by providing clear grounds for relief from the stay and/or sets a time limit for it?

Credit Information in Cambodia – 6 / 8

Under the current methodology the ‘credit information’ accounts for 8 / 20 points of the entire ‘Getting Credit’ score. The 2 gaps in Cambodia’s score are listed below. Collecting and distributing credit information on Firms (#1 below)has been touted for a few years, and is now planned for 2018. The inclusion of retailer and utility company data (# 2) should be in the works.

- Are data on both firms and individuals distributed?

- Are data from retailers or utility companies – in addition to data from banks and financial institutions – distributed?

Summary

The above is not ‘research’ but does raise some interesting points;

- Doing Business report is not intended as a complete assessment of competitiveness or of the business environment of a country. It is a useful proxy for comparing regulatory frameworks across countries. But it is only a starting point for understanding the situation in each country.

- The above illustrates why it is always worthwhile to check if there are outliers that exert particular influence – either positively or negatively.

- Measured by World Bank Doing Business Index, Cambodia has enacted a hugely successful institutional reform (the Credit Bureau of Cambodia). Is it possible to achieve elsewhere?

The 2018 World Bank Doing Business Report for Cambodia is available here.

Comments are closed.