Accessing capital via financial modelling

Our first blog post explained the access to finance experienced by Private Water Operators in Cambodia. This second post details how our financial modelling and business planning helped 20 businesses overcome it. A more detailed description of our work and its success is in this World Bank report.

Introduction

Profitable businesses frequently lack access to finance to grow, whether that be investing in productive assets (fixed assets), or financing working capital and supply chains (inventory). Businesses in Cambodia, as in many other countries, find access to debt finance particularly difficult, as they lack the required collateral (real estate) to secure the loan, and banks lack the capacity to analyse the investment opportunity.

Here we present a case study of a 2014-15 project we undertook with GRET in the piped water industry, to help Cambodian piped water suppliers and banks negotiate improved debt finance to expand network coverage, and therefore Cambodians’ access to safe, piped water.

The project did not use direct grant subsidy to fund the operators’ investments – that’s an expensive and short-term solution to inefficient lending practices. Rather, we focused on how well-constructed investment analysis could influence banks’ credit decisions. Participating businesses paid a nominal fee (to the Cambodian Water Supply Association) to participate and receive our investment appraisal, business planning and other assistance to access financing.

Investment appraisal and financial modelling

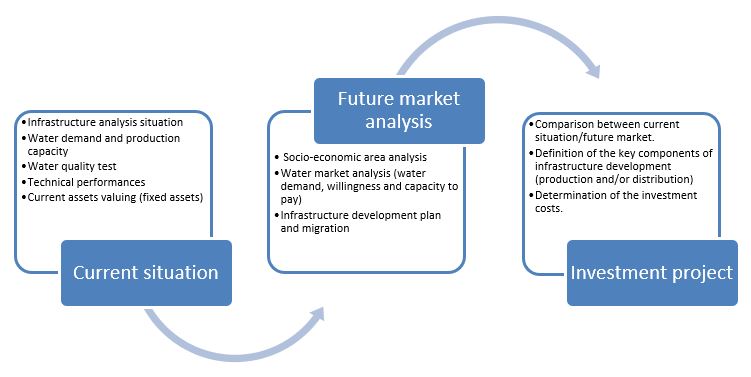

We conducted a preliminary investment appraisal on 29 piped water businesses, from which 20 were selected for more detailed investment study and business planning. The preliminary assessment included analysing the business’s market and their expansion or improvement plans, and a basic financial review and credit analysis. The subsequent detailed study included further technical and market assessment (see diagram below), financial modelling, detailed business planning, preparing the the business for meeting with the bank, and facilitating loan negotiations.

Financial Model

We developed an easily replicable financial modelling tool that allows for quick development of financial forecasts to support financing applications. The contents of the financial model is shown below.

The main objective of financial projection is to provide banks with a long term financial overview of the business to assess their repayment capacity.

The financial projection uses historical data as far as the business can provide it and makes a future projection of 15 years. Projections include an estimate of the income statement, balance sheet and cash flow statement. Sensitivity analysis checks the financial robustness of the business.

The model was structured to minimise the need for individual tailoring of each business, with inputs broken into logical components that flow throughout the model. The process flow of completing the model followed the following path.

Business plan

Comprehensive business plans were developed for the 20 businesses, incorporating: technical and market assessment report; feasibility study report; financial model outputs; and feedback from consultation with the business. Business plans were revised post the lender conducting due diligence. This incorporated recommendations and/or changes required from the lender prior to issuing a loan.

Outcomes

Investments funded and networks expanded

At its conclusion the project was expected to lead to 20 loans signed with a total value of $5.5 million, leveraging $0.5 million in equity. As of December 2015, 9 loans equaling $3.75 million had been formally approved and 5 operators had started construction and 1 operator had completed construction. Investments were mostly geared to expansion of distribution networks (58%), but also a high share were water treatment plant improvements (20%), and 12% were for detailed design and construction supervision.

These 20 investment projects were expected to connect 169,000 additional people by 2020, while a total of 324,000 people would benefit from improvements in water quantity, reliability and quality. This represented improved services for around 10% of the Cambodian population, and an increase in national water access of over 5%.

Furthermore, businesses’ investment plans were based on sound technical assessments and financial models, with qualified supervision during construction as a condition of lending.

Source: Development-Aid

Bank policies and practices changed

EMC also produced a private water sector guidebook. This tool provides an overall understanding of the challenges and opportunities of the sector. It was prepared for banks and other sources of funding. As well as providing a sector overview, it acts as a pitch for the investment quality of piped water operators.

Importantly, in addition to the improved access to finance and expanded piped water coverage, our work resulted in a change in bank lending policy and practices for piped water operators. Close dialogue with banks resulted in the development of a streamlined protocol for screening, due diligence and delivery of a tailored loan-product for the water supply sector – one no longer based on hard-collateral.

The major change was banks accepting soft titles, water infrastructure assets and the NPV of existing cash-flows as collateral[1]. This was a major development in improving access to finance for Cambodian businesses.

[1] 50% of the NPV of cash flows generated by existing water schemes based on 10 year projection at a 15% discount rate.

Other relevant EMC blog posts include:

Borrowing capacity of Cambodian businesses

Comments are closed.